Mass Retirement For Boomers Adds Urgency To Insurance Talent Search

The Risk Institute at The Ohio State University Fisher College of Business recently released data from its Fifth Annual Survey. Ninety-five percent of firms reported impending impact due to the mass retirement of baby boomers, with 60% saying it will have a high to moderate impact.

March 24, 2020

Education & Training

Risk Management

Reputational Damage: Insurance Faces A Crossroads In Post-Coronavirus World

Right now, in the midst of the COVID-19 crisis, it is tough to imagine the fertile environment for insurtech start-ups that the sector has enjoyed can last much longer. The crunch from social distancing, if not out-and-out restrictions on economic activity, will undeniably freeze the flow of cash to untested ideas.

March 24, 2020

Catastrophe

Risk Management

Cybercriminals Exploiting COVID-19 To Spread Their Brand Of Viruses

The mounting threat of COVID-19 has placed the healthcare system of many nations under a huge amount of pressure, and cybercriminals could be exploiting this to spread viruses - but instead of biological ones, these are computer viruses.

March 20, 2020

Life & Health

Risk Management

Technology

How To Lead And Collaborate In Claims

Much has been written over the years about what sets great claims organizations apart from all others, but none of these analyses really apply anymore.

March 18, 2020

Education & Training

Risk Management

End Of Days, Part 1: With Everything Cancelled, Why Are We So Busy?

Perhaps it was just plain ignorance. It might have simply been complacency. We have, after all, survived the end of the world a number of times. But this one caught us by surprise. Who knew that there would be so much to do during the COVID-19 end of days?

March 17, 2020

Risk Management

Claims Management And Effective Risk Management

The nature of mature, and by inference effective, risk management programs has claim management as a key focus as well. While risk maturity is directly correlated with risk effectiveness, this latter term encompasses a much broader perspective on things that matter.

March 17, 2020

Education & Training

Risk Management

RIMS Cancels 2020 Convention Amid Coronavirus Spread

The Risk & Insurance Management Society Inc. on Monday canceled its annual conference due to be held May 3-6 in Denver amid the new coronavirus epidemic.

March 16, 2020

Risk Management

Employers Balance Coronavirus Disclosure with Privacy

Numerous privacy lawyers tell us they’re seeing a growing number of frantic requests from employers about disclosure protocol related to the coronavirus outbreak.

March 13, 2020

Life & Health

Risk Management

Measuring Productivity In The Age Of Smartphones

Do you remember the good old days? Back when it was easy to measure your team’s productivity by the number of cars in the parking lot. If you came in at 7:30 am, and the parking lot was full, things were probably flowing well. If you left at 5:30 pm, and the parking lot was still full, you could be certain it was a productive day.

March 13, 2020

Risk Management

Hackers Pounce as Coronavirus Spread Triggers Work-at-Home Movement

As businesses increasingly—and in rapid fashion—urge their employees to stay at home to work amid the coronavirus pandemic, another risk to companies is emerging. Cybersecurity experts warn that cybercriminals are moving in to target people not used to working from home and companies without work-at-home policies or cyber-safety nets.

March 13, 2020

Risk Management

Technology

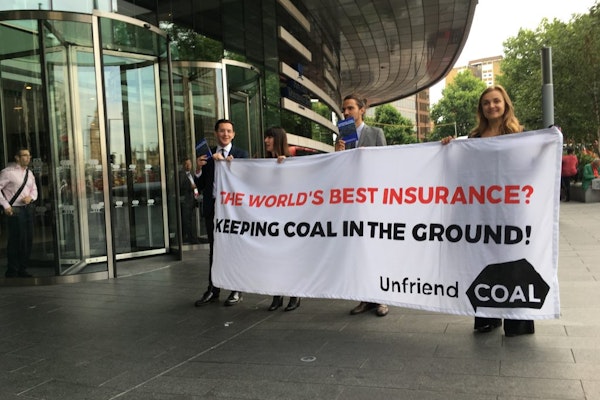

In Battle Of Climate Activists Vs. Insurers, Who Will Be Left Standing?

From coal mines to fossil fuels and oil sands, the insurance industry is facing increasing pressure from activists, the public, and its own employees to move away from industries whose activities are purportedly causing environmental harm.

March 12, 2020

Risk Management

Risk Managers Advised To Prepare For Coronavirus D&O Claims

Businesses should brace themselves for a likely flood of shareholder suits related to the new coronavirus outbreak, but the success of any litigation may depend on companies’ willingness to fully disclose directors and officers liability-related risks now, say many experts.

March 10, 2020

Liability

Litigation

Risk Management

Data Security To Be Found In The Cloud

As the insurance industry continues down the path toward digital transformation, it is being inundated with data being generated by many different connected devices and systems. Enterprise data is growing so rapidly that analysts at IDC predict the worldwide volume of data will increase ten-fold to 163 zettabytes by 2025.

March 9, 2020

Risk Management

Technology

7 Ways Diversity and Inclusion Are Positively Impacting Insurance

In recent years, efforts to promote diversity and inclusion in insurance and other industries have become increasingly structuralized, hardwired into most companies’ business models.

February 26, 2020

Education & Training

Risk Management

Flipping The Narrative In An Industry Of Endless Possibilities

The current insurance industry is in a quasi-crisis in terms of talent. Over the next couple of years, there will be a mass exodus of legacy insurance professionals which will create a vacuum that must be filled by young talent. The talent gap stats have been blasted all over insurance articles so I will refrain from regurgitating that data here as the point of this article is deeper than statistical analysis.

February 26, 2020

Education & Training

Risk Management